What once seemed like a step into a weekend dream: bustling food halls, lively cinema halls, bags in hand after a shopping spree, now rings strangely hollow. Enter today, the lights are still on, the escalators are still moving… but where is everyone?Welcome to the ghost malls of India, where you’ll find stores still open, food stalls still serving, but somehow, that’s still not enough to attract crowds again.

This is the reality for nearly 20% of malls across India. The once-bustling hangouts began to quietly lose their charm, fading into an eerie silence.But how did places that were always crowded suddenly become so quiet?Today, nearly one in five malls in India are underperforming or nearly empty, according to a report by Knight Frank India. With the retail world divided into thriving spaces and struggling spaces, these “fake malls” are not just a sign of what has gone wrong, but also an opportunity to rethink and reinvent how these spaces are used.

While some malls still pulse across India’s urban skyline, others are losing importance, with fewer shoppers and more closed stores. Its decline shows how India’s retail market is changing: it’s no longer just about space, it’s about delivering the right experience in the right place.

A haunting issue: 74 malls, 15.5 million square feet, and a lot of silence

Today, India is home to dozens of distressed or closed malls, especially in metro suburbs and small cities that saw the first wave of mall construction in the 2000s. The numbers almost seem like a warning sign.

Of the 365 malls surveyed across India, 74, nearly 20%, were classified as “fake malls”. Together, this represents about 15.5 million square feet of vacant or underutilized retail space, a lot of space designed for shoppers who no longer show up.

These are not just struggling malls with a few closed stores, they are retail spaces that have lost their commercial pulse, as a high vacancy rate, poor footfall, and a broken tenant mix have rendered them irrelevant.What makes these malls even more worrying is what they once promised. They were built as symbols of aspiration, at a time when malls represented modern India, exquisite interiors, international brands, food courts, cinemas and weekend family outings. At that time, these centers were not just shopping centers; They were signs of an emerging urban lifestyle. Today, many of them stand as quiet reminders of what happens when real estate ambition moves faster than retail reality.

Where Ghosts Live: West and South dominate the Dead Space map

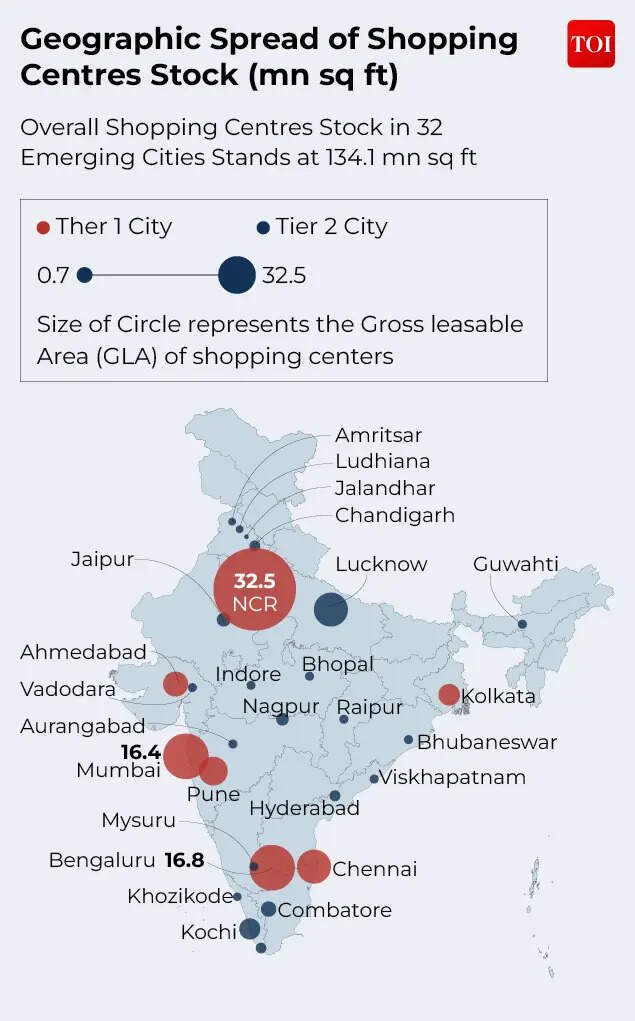

If you were to map India’s abandoned malls, the geography of dead space is not evenly spread. West and South India dominate the list. These areas represent the largest concentration of distressed or nearly dead mall assets.This in itself provides a strong narrative hook. Why do “ghosts” gather there? In many cases, these were among the oldest and most aggressive mall development markets. Cities in the West and South saw rapid construction of shopping centers during the great retail real estate boom, when developers rushed to monetize urban land and consumers became optimistic.

But size alone does not guarantee sustainability.

Why are malls dying?

The rise of fake malls in India is less about a decline in consumer spending and more about poor planning and oversupply in certain areas. Many malls, especially in the same area, lack differentiation, causing fragmented footfall and frequent store closures. E-commerce has accelerated this decline, but it is not the main reason. “India’s ghost malls are less a reflection of weak consumption than a result of uneven expansion in supply and gaps in asset positioning across smaller markets.

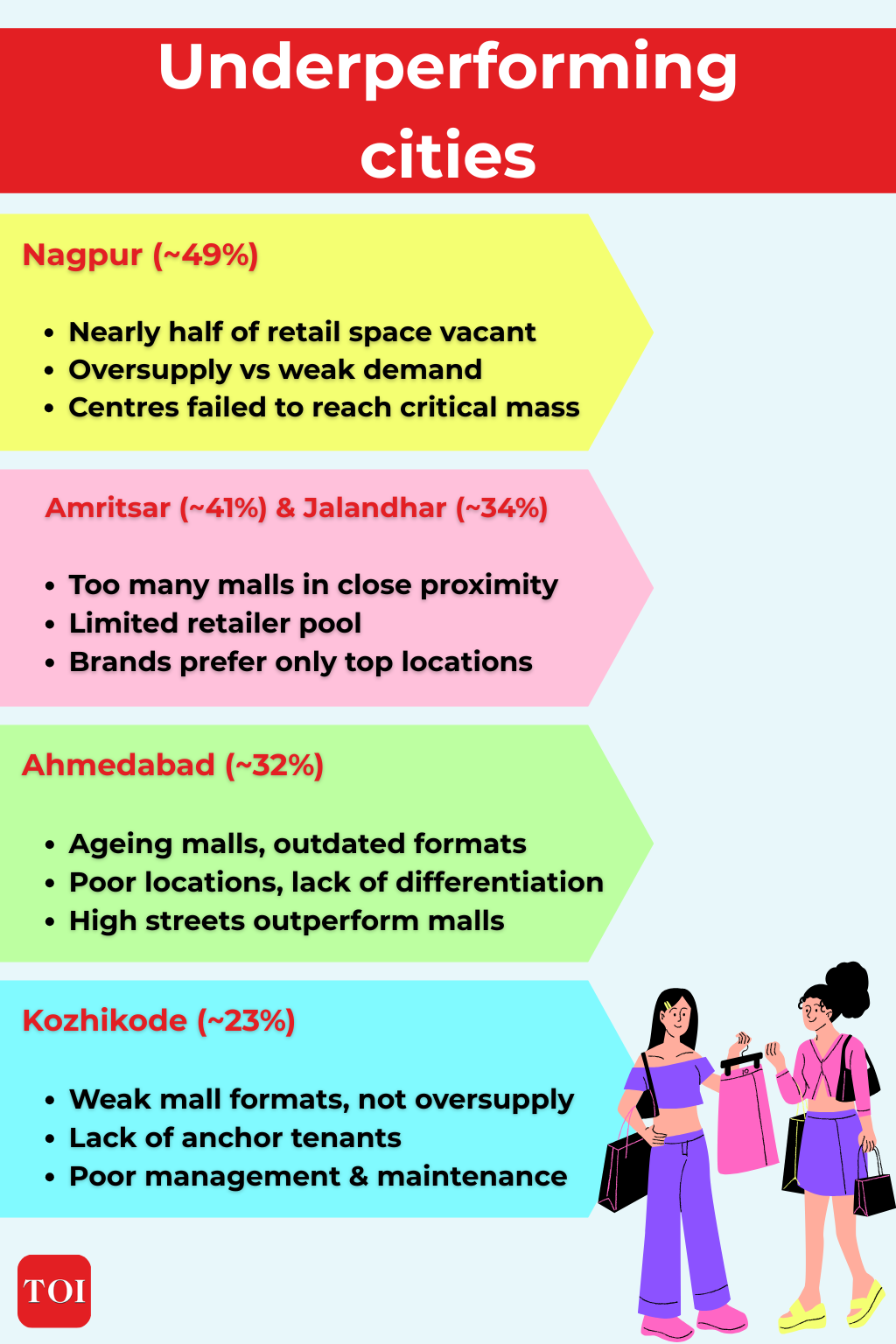

Nearly 20% of malls in over 30 cities are currently experiencing under-occupancy, with pressures evident not only in smaller towns but also in pockets of larger urban markets,” Navin Malpani, partner and head of consumer and retail, Grant Thornton Bharat, told TOI.When the location is wrongOne of the biggest factors behind a mall’s success is its location, which ironically is often the thing that leads to its downfall. Poor planning in the beginning, such as choosing the wrong area or misjudging demand, has turned many malls into ghost spaces.

Many shopping centers are built in areas that do not have a sufficient consumer base to support them. In small cities, developers in the 2000s sometimes overestimated future demand, building multiple malls where just one would have sufficed, leaving several malls half-empty from the start.

In other cases, too many malls have sprung up in the same area, all vying for the same spotlight. When supply exceeds demand, only a few malls remain relevant, while others slowly lose popularity. Take Noida’s Great India Place, Wave Mall and DLF Mall of India. Being located close to each other and targeting the same shoppers, the arrival of the larger, modern DLF Mall of India has changed consumer preferences, leaving older malls struggling to keep up the pace.

During my time in Noida for graduation from 2016 to 2018, Great India Palace (GIP) was everyone’s hangout. We would meet there to decide on movies, food and shopping. Later, the Mall of India gained popularity, but the GIP remained widely available ministerially. People often visit both malls to compare which one is better for watching movies, shopping or eating. Over time, some stores in GIP began to close, and footfall gradually moved to other places. The Wave Cinema at GIP still attracts a few visitors, but apart from that, activity has slowed. The GIP has been central for many years, especially in the late 2010s, but since around 2022-2023, post-pandemic lockdowns and slowdowns have gradually changed its importance.

Harsh Shivam, a former engineering student, told TOI.

Aging malls that haven’t agedDo you remember the old mall you used to visit when you were a kid? Yes, this center may also have become a ghost mall today. A number of first-generation malls from the early 2000s have failed to keep pace with changing consumer tastes and expectations.

As shiny new complexes opened elsewhere, older centers that had not renovated, modernized or reinvented themselves saw their patrons slowly move away. As newer, flashier malls came on the scene, those stuck in the past lost visitors, unable to compete with modern designs, better lighting, and more engaging experiences.

MG Road malls in Gurugram are a classic example, once the city’s retail district but gradually losing favor to newer destinations like CyberHub and the malls along Golf Course Road.

Today, shoppers are looking for more than just stores, they want experiences, entertainment and immersive atmospheres, making… It is difficult for older malls to attract repeat visitors.A lot of mall owners screw upHave you ever wondered why some malls are unresponsive? Many of India’s underperforming malls suffer from fragmented ownership. Here’s what happens: During construction, developers often sell individual store units to several investors to raise money. Sounds smart, right? But the problem is that without a single entity managing the mall, maintaining high quality standards and organizing the right mix of tenants becomes nearly impossible. Each store owner rents their space to whoever will pay, resulting in a haphazard mix of stores, inconsistent storefronts, and a lack of coordinated marketing. The result? Instead of being a vibrant, cohesive shopping destination, the mall begins to feel like a collection of small, unrelated stores. As shoppers notice the chaos and lack of experience, shopping demand declines. So, next time you visit a mall that feels disjointed, fragmented ownership may be the reason!

When the main stores come outAnchor tenants, such as movie theaters, supermarkets, or big-name brands, are the lifeblood of a mall. They attract crowds, and small shops thrive on this traffic. But what happens when a major anchor goes out? Footfall drops sharply, small retailers begin to suffer, and soon a domino effect begins. Sales decline, stores close, and the once-bustling mall begins to feel empty and abandoned. The effect can be devastating: the departure of one anchor can threaten the viability of the entire center.

Without a quick replacement, other tenants follow suit, vacating their places and leaving the mall as the number of visitors dwindles. In many cases, this chain reaction has been deadly, turning once vibrant shopping destinations into ghostly corridors. Essentially, when the big draw leaves, the entire ecosystem suffers and the once-bustling mall can quickly become a hollow shell.E-commerce has changed the rules of the gameDemand for shopping centers is also declining due to the rise of e-commerce over the past decade. These malls often rely on stores that sell books, music and basic electronics, categories that shoppers now prefer to buy online. Without unique experiences or exclusive offers, what real reason do people want to visit? Maybe a food court or a cinema, but even these are not enough if the mall location is poor or uninspiring.

Then came the COVID-19 pandemic, and things got worse. Already financially struggling malls could not withstand months of closure, and many never recovered.

Legal problemsSometimes, it’s not just design or competition, but external management issues that can destroy a shopping center. Projects facing protracted legal disputes, such as land ownership disputes, zoning issues, or delays in certificates of occupancy and approvals, often struggle to lease space effectively, leaving buildings empty. Take the Grand Sigma Mall in Bengaluru as an extreme example: legal issues over land use meant it could never fully open, and it was eventually demolished, resulting in a complete loss of value. Even well-designed and strategically located malls can falter if regulatory hurdles are not resolved quickly. Such compliance failures scare away retailers and visitors alike, turning promising projects into dead assets. Shopping centers “die” when their core value collapses, whether due to faulty location, poor management, loss of consumer confidence, or broader economic pressures.

Quality over quantity: Retailers focus on efficiency and expertise

Retailers are now prioritizing efficiency and performance, reconsidering leases, downsizing poorly performing stores, and converting outlets into experience or fulfillment centers. India does not lack demand; Instead, consumers are choosing quality and convenience.” For retailers, this has led to an increased focus on store-level productivity and capital efficiency, with renegotiated lease structures, rationalization of store networks, and the use of physical stores as experience and fulfillment centers.

Ultimately, India is not suffering from a demand deficit, but rather experiencing a filter of quality and convenience. “It is clear that the market is split between high-performing, curated retail destinations and commodity assets that are becoming increasingly obsolete,” Malpani told TOI.

The great contrast: empty malls in a market suffering from a shortage of retail space

This is where the story gets really cool and a little silly.India has ghost malls, but there is a shortage of quality mall spaces.At first glance, these two facts should cancel each other out. If there is empty retail space, why do brands keep saying there isn’t enough space? Why are rents in major malls strong? Why are newcomers still struggling to find the right location?The answer is simple and powerful: not all retail spaces are created equal. It is this contradiction that makes the story of the Ghost Center more than just a story of collapse. India does not have a pure oversupply problem.

It suffers from a mismatch problem. There’s dead space, yes, but it’s often in the wrong place, with the wrong layout, the wrong mix of tenants, the wrong watershed, or the wrong consumer offering.

Millions of newly affluent consumers are driving demand for Louis Vuitton, Chanel, Dior, and others. However, India has only a very few luxury malls: Emporio and Chanakya in New Delhi, and Jio World Plaza in Mumbai.As Saurabh Bharara of DLF told ET, major global brands are keen to enter India, but quality space is scarce. Luxury retail requires more than just square footage, it requires the right ambience, engaging tenants, consumer profile, parking and proven footfall. An empty unit in Met Mall is not an opportunity, it is a risk. The challenge is not the excess space, but the right space.Why? Because luxury doesn’t just need square footage.

It needs context.

The silver lining: Dead malls can be born from Jedi D

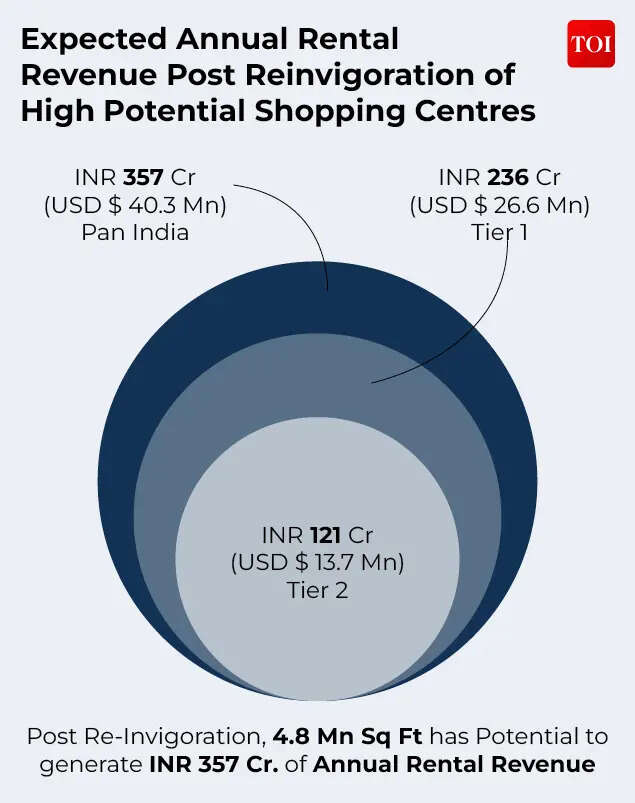

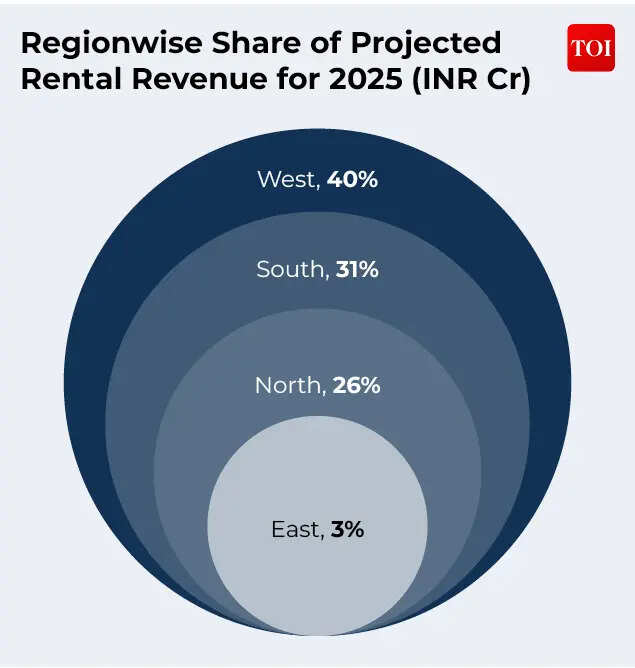

Not every ghost mall has to remain a ghost. So, what should the city do with 15.5 million square feet of empty retail space? Imagine transforming old, quiet malls into bustling hotspots and generating strong returns while doing so. This is exactly the opportunity available in the retail real estate sector in India today. Tier 1 cities have two-thirds of the potential (INR 236 lakh crore), while Tier 2 cities add another INR 121 lakh crore. Instead of spending huge sums on building new malls, investors can revive dormant centers and unleash cash flows through expected rental yields of 5.86%.Regionally, the West and South dominate, generating 77% of expected rental income. But the trick is in the strategy: choose the right property, execute it well, and these “sleeping giants” can be turned into high-yielding, value-added investments. Lessons from global markets show how revitalization works, and in India, 15 shortlisted centers in 11 cities can together generate Rs 357 Cr annually.It’s not enough to just add some new branding, a fresh coat of paint, or a new logo.

True revitalization often means rethinking the purpose of a space, resizing it, re-leasing it, improving circulation, enhancing access, or even transforming the mall into something entirely new.

Beyond shopping: entertainment centersTurn the mall into a playground! Empty units can become amusement parks, arcades, bowling alleys, or sports facilities. Young people and families get an ‘everyday’ experience, while remaining retail stores and cafes benefit from the extra footfall.Retail Revival: Upgrading and RepositioningSome malls just need to be renovated. Modern interiors, better layouts, new flagship stores, trendy cafes and entertainment options can keep shoppers coming back. Marketing helps reposition the mall as a must-visit destination.Reimagining the Workplace: Coworking HubsFake malls with large spaces, parking lots and central locations can become co-working centers. Startups, small businesses, and corporations are always looking for flexible spaces. According to Knight Frank, even food halls and entertainment areas can be transformed into lounges, meeting spaces or event areas.

Suddenly, an empty mall began to bustle with professionals instead of shoppers.Learning under one roof: education facilitiesMalls can be your new classroom… literally quiet! Large, accessible spaces can host training centres, skill development institutes, or even affiliated universities. Empty shops can be converted into classrooms, auditoriums and administrative offices. With parking and transportation already in place, these centers can attract students throughout the year, especially in tier-II cities where quality education is limited.Hospitalization spaces: healthcare centersGhost malls are ideal for clinics, diagnostic laboratories, pharmacies or even small hospitals. Its layout, parking and multiple entrances make it ideal for patients and visitors. Medical tenants bring stable leases, while communities gain better access to healthcare.Rebuilt to fit: mixed-use redevelopmentWhen retail alone doesn’t work, consider mixed use. Offices, schools or medical facilities could occupy part of the mall, or in extreme cases, the entire structure could be rebuilt for a new purpose.

Empty spaces can finally have their place.

Bottom line?

The story of India’s abandoned malls is not just about empty corridors and silent food courts, it is a lesson in adaptation. While many first-generation malls failed to evolve with changing tastes, their vast spaces, central locations and existing infrastructure hold enormous potential. From entertainment centers and co-working spaces to educational centers and healthcare facilities, these “sleeping giants” can be reinvented to meet today’s urban demands.

For investors and cities alike, the message is clear: with the right strategy, what once seemed empty can be transformed into vibrant, profitable destinations. Yesterday’s malls may become tomorrow’s thriving landmarks.Takeaway? There is a ‘second chapter’ ready to be written in retail real estate in India, and yesterday’s malls may become tomorrow’s cash cow.