")

To understand the scale of change, it is useful to reconsider how salaries are typically paid in India. (Amnesty International image)

The wage and compensation landscape in India is entering a new and progressive phase. The implementation of the four labor laws, effective November 21, 2025, along with the new income tax law and rules that will take effect April 1, 2026, represents a coordinated effort to modernize how salaries, benefits, and social security are administered.At the heart of this shift lies a uniform definition of “wages” under labor laws – a seemingly simple reform that brings consistency and transparency to pay structures that have evolved over decades. This shift is expected to strengthen the relationship between profits, legal benefits and long-term social security. At the same time, the proposed revisions to income tax exemption limits are expected to enable employees to claim higher tax credits on select bonuses and benefits, improving the overall treatment of compensation.In this environment, employers must carefully balance the definition of wages under employment laws and revised income tax rules, while assessing the impact on compensation arrangements. The various components of pay now need to be reviewed through legal and tax lenses, requiring organizations to re-evaluate the implications for costs, benefits and competitiveness.

How salary structures have traditionally worked

To understand the scale of change, it is useful to reconsider how salaries are typically paid in India.

Most organizations follow the cost to company (CTC) model, under which total compensation is divided across multiple components. These usually include basic salary, allowances such as House Rent Allowance (HRA), special allowance, transport allowance, employer contributions to provident fund and other benefits.Over time, many employers adopted compensation models where a portion of the CTC was paid as base salary, with the balance distributed through allowances and compensation.

This approach served two broad purposes. Firstly, it limited the basis on which statutory contributions such as provident fund and gratuity were calculated. Second, it often boosts employees’ wages in the short term, especially when some allowances or compensation enjoy tax breaks.

Labor laws and the new definition of wages

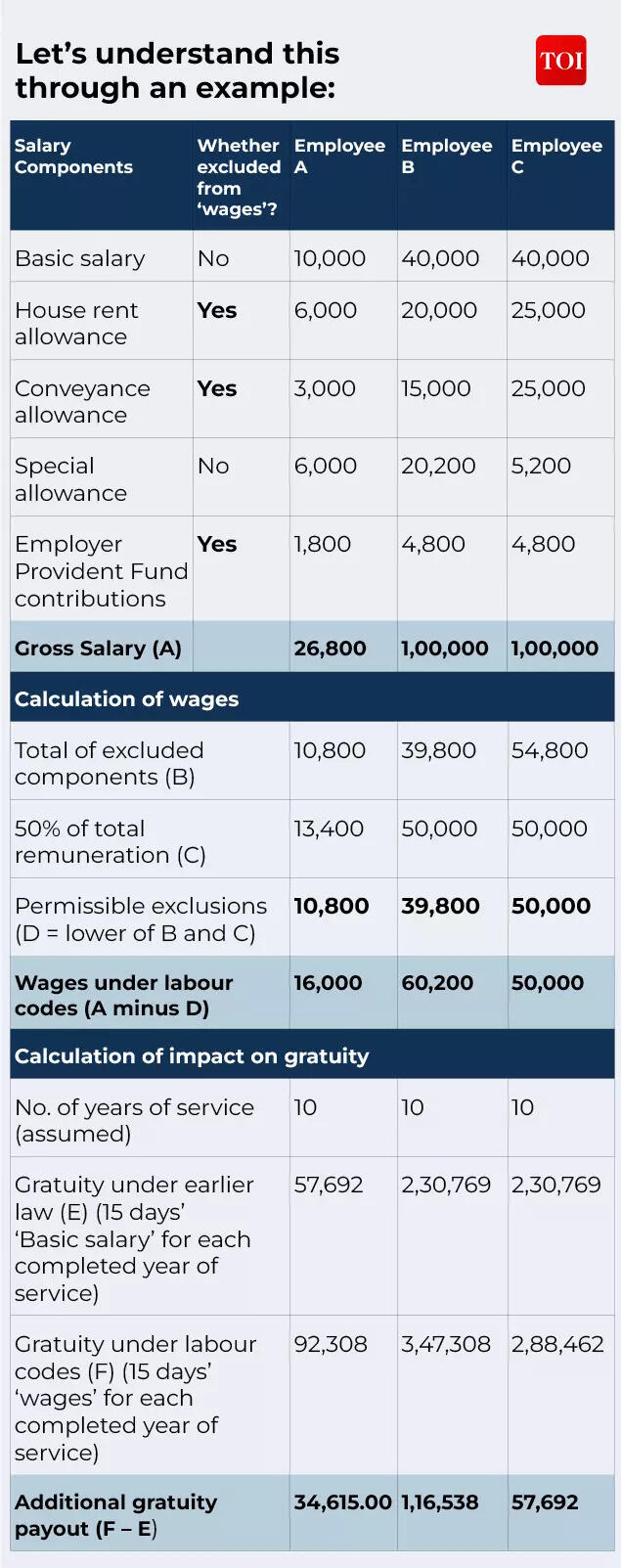

Labor laws seek to replace this variation with greater uniformity. Under the new framework, the definition of wages has been standardized across all four laws, creating a single reference point for calculating statutory benefits.Wages broadly include all remuneration payable for work, subject to specific exceptions such as house rent allowance, transportation allowance, statutory remuneration, commissions, specific compensation and retirement benefits. Any element of the salary that does not fall within the established exceptions may be treated as wages.The main feature of the frame is the introduction of a structural threshold. Excluded items may not exceed 50% of gross pay.

If this limit is violated, the redundancy is automatically included in wages. This effectively determines the minimum wage-related components such as basic salary, dearness allowance and other included elements.The intention is to reduce excessive wage segmentation and ensure that social security contributions are calculated on the basis of more representative earnings.It is also important to address a common misconception. Even organizations where base salary is set at 50% of gross pay may be affected.

Where components such as special bonus form part of gross pay arrangements, it may still be necessary to include them within wages, depending on how the gross remuneration is constituted.

Interaction with new income tax rules

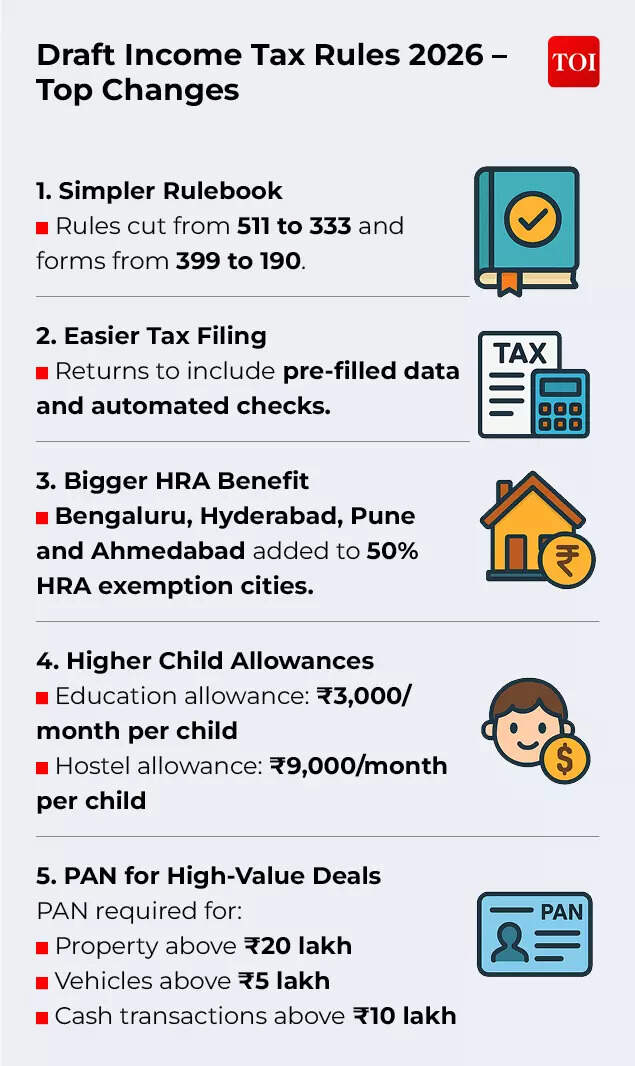

On 7 February 2026, the draft Income Tax Rules 2026 were put out for public consultation, marking significant changes to the tax treatment of certain allowances and benefits.As per the proposed rules, when an employee owns a vehicle and uses it for both official and personal purposes, the tax exemption limit for operating and maintenance expenses borne by the employer has been increased to Rs 5,000 per month (plus Rs 3,000 per month for the driver, if provided), from the existing limits of Rs 1,800 and Rs 900 respectively.

Higher limits apply to vehicles with larger engine capacity. Corresponding increases have been made to taxable base values where cars are owned or leased by employers.The exemption limit for free food and non-alcoholic beverages served during working hours – whether in office premises or through paid vouchers – has been enhanced to Rs 200 per meal, up from Rs 50.The list of cities eligible for 50% HRA exemption under the old tax regime has been expanded beyond the four metros to include Bengaluru, Hyderabad, Pune and Ahmedabad.

The exemption limit for child education allowance under the old tax regime has been increased to Rs 3,000 per month per child (from Rs 100), subject to a maximum of two children.The interaction between labor laws and the income tax framework also needs to be viewed in the context of the old and new tax systems. For example, HRA is specifically excluded from the definition of wages under labor laws. From a tax perspective, an HRA may be partially exempted under the old tax regime, subject to prescribed conditions, while remaining fully taxable under the new tax regime.

Similarly, the revised income tax rules provide for a cap on tax exemption on free food and non-alcoholic beverages, including meal vouchers, while the draft central rules under labor laws propose to exclude meal vouchers from the definition of wages.

These examples illustrate that the tax treatment of a component and its treatment under labor laws can differ, and that both frameworks operate independently, but in parallel.

Impact on bonuses and provident fund contributions

The revised definition of wages has important implications for Social Security. Benefits such as severance pay and holiday pay will now be calculated based on the new wage definition, which may increase employer expenses as the wage base expands.However, provident fund contributions remain unchanged for now. Provident Fund contributions may continue to be calculated on the basis of the statutory maximum wage of Rs 15,000 per month, or such revised ceiling as may be notified under the Provident Fund Scheme.

Employers and employees may continue to contribute 12% of basic salary when basic salary exceeds the maximum, even if wages under labor laws are higher. This ensures continuity and avoids an automatic reduction in the wage collected solely due to the new definition of wages.

Transition management

From a compliance perspective, introducing a uniform definition of wages reduces ambiguity and interpretive disputes, especially for organizations operating across multiple states.

At the same time, employers will need to assess the financial implications arising from higher statutory wage benefits and ensure that systems, payroll processes and HR platforms are compatible with the new framework.An important guarantee is provided during This transfer is under Section 124 of the Social Security Law. This provision prohibits employers from reducing an employee’s wages or benefits solely because of increased statutory contribution requirements.For employees, the changes provide greater clarity on how different pay components are treated for statutory benefits and tax purposes, enhancing transparency around earnings and Social Security coverage in the long term.Looking forwardAs the central and state governments finalize the supporting rules and accelerate the pace of implementation, the practical impact of labor laws will become clearer. In the near term, proactive planning will be critical to managing the transition smoothly.In the long term, India’s new wage framework represents a structural shift towards greater consistency, predictability and harmonization of labor and tax laws. By strengthening the link between income and social security while allowing appropriate tax relief on selected benefits, the reforms represent an important step in the evolution of the world of work in India.(Puneet Gupta is a partner in People Consulting Services Tax at EY India)