")

With another tax filing season approaching, it’s important for taxpayers to plan. (Amnesty International image)

The personal tax compliance framework in India is witnessing a decisive transformation, driven by digitization, integration of pre-filled data, and introduction of simplified tax regimes by the Indian Income Tax Department.The Income Tax Returns (ITR) forms for the financial years 2025-2026 (AY 2026-2027) underscore this development, marking a shift from basic disclosures to more stringent requirements for accurate, consistent and comprehensive reporting by taxpayers, helping authorities to quickly navigate the expedited processing of tax returns as cross-verification of claims between individual income tax returns against reports from businesses becomes easier.With another tax filing season approaching, it’s important for taxpayers to plan.

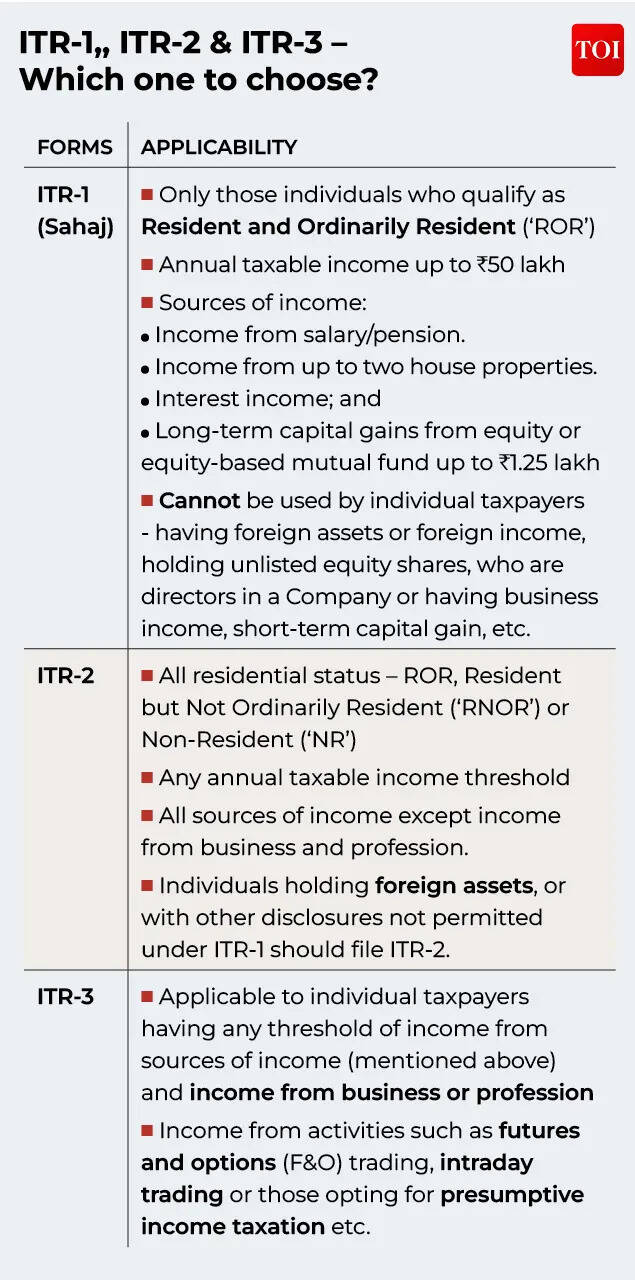

The first question that arises is which ITR form you can choose from among the various forms notified by the tax department. Choosing the appropriate ITR form depends on the specific circumstances of the individual, including residence status, nature of income, taxable income limits, etc.Against this backdrop, a thorough understanding of the various ITR forms for FY 2025-26 is essential for globally mobile professionals, local salaried taxpayers and individual investors to understand the basis of the applicability of the different ITR forms.

Please refer to the table below.

ITR-1, ITR-2, ITR-3 – which one to choose?

Please refer to the table on selection criteria for selecting appropriate ITR forms:

Submitting an ITR under an incorrect form may be considered defective, which may result in delay in processing and follow-up procedures from the tax department. This remains a common mistake in practice. For example, salaried taxpayers who also engage in F&O trading activities often mistakenly file an ITR-2, even though they are required to file an ITR-3 due to the presence of business income.

This misclassification may complicate compliance and necessitate revision of the International Telecommunication Regulations.Given the increasing complexity of income profiles, individual taxpayers should carefully assess the nature and sources of their income before selecting the applicable ITR form to avoid procedural setbacks.

Residential Status – Does it affect the selection of ITR form?

Individual taxpayers who qualify as an RNOR or NR are not eligible to file an ITR-1, regardless of their sources of income.

In such scenarios, taxpayers are usually required to file an ITR-2.Taxation on non-residents is limited to income received in India, deemed to be received in India, or income which accrues or arises in India. However, with the increasing prevalence of remote working and cross-border employment arrangements, determining the source of income and its taxability has become quite complex.In addition, non-resident taxpayers are required to make enhanced disclosures in their ITRs, including details such as their country of residence, Tax Identification Number (TIN), period of stay in India, etc. Therefore, accurate determination of residency status at the outset is essential to ensure correct reporting and selection of the appropriate ITR form.

Old personal tax regime vs new personal tax regime – Can I reconsider my tax regime in ITR?

Taxpayers who are effectively salaried have two opportunities to evaluate their choice of personal tax system. First, at the beginning of the year when preferences are communicated to the employer for withholding purposes, and again after the end of the year at the time the ISA is filed.ITR forms require taxpayers to explicitly confirm their chosen regime at the time of filing. NPTR continues to apply by default, while the Old Personal Tax Regime (‘OPTR’) option requires active selection. It is worth noting that for salaried individuals, the choice made at the time of application may differ from the choice declared to the employer during the year.Given that the chosen regime directly impacts the availability of deductions and exemptions, taxpayers should undertake a careful re-evaluation process before finalizing their ITRs.In cases where OPTR is chosen, it is essential to ensure that all deductions and exemptions are accurately reported and supported by appropriate documentation, especially given the increased system-based validations and cross-verification of data by the tax administration based on reports from corresponding companies and information collected from other sources.

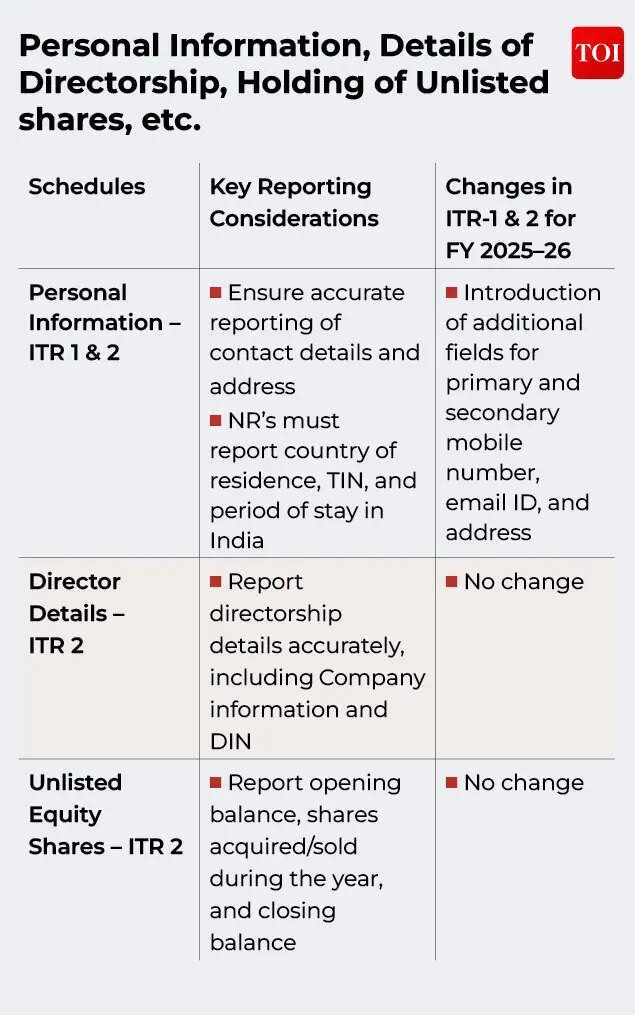

ITR Tables – How to navigate the reports?

Now that we understand the ITR selection criteria, let us now delve deeper into the models and analyze the schedule reporting requirements.

This serves the purpose of collecting basic information and documents that individual taxpayers may need while filing ITR forms. We have tried to divide the illustrative list below according to the subject of the required reports in the tables for ease of reading and understanding.

However, it is recommended that you consult an expert on the subject before filing your tax return.Personal information, management details, holding of unlisted shares, etc.The first section of the IFR model focuses on the taxpayer’s basic information and applicability-related disclosures that form the basis of the filing. Accurate reporting of personal details, management positions and unlisted share contributions is crucial, as these disclosures are increasingly being used for system-based validation checks by the tax administration.

Report sources of income under different headingsWith increased integration between AIS, TIS and TDS disclosures and system-based validations, taxpayers must ensure that income is properly classified, reconciled and disclosed under the appropriate timelines.

| Timetables | Key reporting considerations | Changes in ITR-1 and 2 for FY 2025-26 |

| Salary scale – ITR 1 and 2 | Ensure consistency between Form 16 and the Annual Information Statement (AIS)/Taxpayer Information Summary (TIS) available on the Income Tax Portal Accurately report the bifurcation of salary income into allowances, bonuses and deductions Maintain details of House Rent Allowance exemption claimed (rent paid, metro vs non-metro classification, landlord details) Salaried individuals who have income from foreign retirement accounts (such as offshore pension or Social Security plans) should carefully evaluate taxability and maintain supporting documentation. Form 10-EE must be filed if tax deferral is elected for income from foreign retirement accounts | The ITR-1 no longer allows reporting of income from foreign retirement accounts where tax deferral has been elected |

| Home Ownership Schedule – ITR 1 and 2 | Maintain ownership details including ownership share and PAN number of the co-owner and TF The original tenant Maintain complete home loan documents, including loan account details, outstanding balance, interest, etc. | The ITR-1 now allows reporting of income from up to two homes Accordingly, additional details are required, including the property address, co-ownership details, ownership percentage, co-owner name and Personal Identification Number (PAN), and tenant details. Unrealized rent can now be claimed as deduction, and net rental income will be reported in ITR-1 There is no change in reporting requirements in ITR-2 |

| Schedule of capital gains – ITR 1 and 2 | Capital gains remain a key area of audit, requiring transaction-level accuracy and reconciliation with AIS and broker data Proper classification of short-term and long-term capital gains is imperative All capital transactions should be reported, including those where gains may ultimately be exempt or below the taxable limit. For example, long-term listed equity gains within the exemption limit of INR 1,25,000 or gains fully offset by available losses | Removed dual-period capital gains calculation requirements as they were only applicable to FY 2024-25 as a transition year. |

| Virtual Digital Assets (VDA) – ITR 2 | Report transaction details for each transfer of cryptocurrencies/other VDAs, including acquisition date, transfer date, sale consideration, and acquisition cost The loss resulting from one VDA transaction cannot be offset against the gains of another VDA or any other income No deduction other than acquisition cost is allowed while calculating VDA taxable income | No change |

| Tabulation of other sources – ITR 1 and 2 | Report income on a gross basis Proper classification of interest based on source, such as savings account, fixed deposit or interest from provident funds, companies and financial institutions | Introduction to additional fields for reporting benefits earned from: Non-banking financial companies Housing finance companies Companies Specific bonds or loans subject to concessional interest rates obtained by non-resident representatives |

Filing, posting losses, reporting exempt income, deductions, etc.This requires careful attention, especially since the ITR utility now performs enhanced checks between schedules and verification of pre-populated information. Inaccurate claims, incorrect clearings, or incomplete disclosures may result in denial of benefits, validation errors, or processing delays.

| Timetables | Key reporting considerations | Changes in ITR-1 and 2 for FY 2025-26 |

| Loss Clearing and Carriage – ITR 2: Current Year Loss Adjustment (CYLA) Bringing Loss Adjustment (BFLA) Loss carry forward (CFL) | Ensure losses are reported under the correct income heading and year of assessment, as the facility requires an annual breakdown of carry-forward losses Reconcile the carry forward losses with the previous year’s ITR to avoid any mismatch Verify that losses being offset qualify against the relevant capital income (for example, capital losses can only be offset against capital gains subject to applicable rules). Note that some losses cannot be carried forward unless the original return is filed within the ISA filing deadline | No change |

| Chapter VI-A Deductions – ITR 1 and 2 | Life insurance premium/other eligible investments, maintaining details like policy/policy number, name of institution/insurance amount invested/paid etc. Repay the housing loan principal, maintain lender details and loan account information Medical insurance discount, keeping the policy number, name of the insurance company, details of the insured person, and the amount of premium paid. National Pension System (NPS) contribution, maintaining account details/PRAN and contribution amount Ensure that deductions are not duplicated i.e. additional claims are not filed in the ITR when the employer has already considered them in Form No. 16. | Section 80G: Additional disclosure is now required for payment details like transaction reference number (UPI/check/NEFT/RTGS) and IFSC bank code while claiming donation deduction Section 80GGC: Additional disclosures now required for name and PAN of political party/electoral fund while claiming deduction for political contributions |

| Exempt Income Schedule – ITR 1 and 2 | Check the correct classification of exempt income from the drop-down list available Exemptions based on the avoidance of double taxation agreement such as dependent personal services, short stay exemption, etc. must be reported in this table and the disclosure of the availability of a tax residence certificate must be marked | Clarify that the treaty-based exemption only applies to non-authorised countries |

Reducing foreign taxes, reporting foreign income, foreign assets, and asset and liability balancesThe comprehensive exchange of information regarding overseas income and assets between governments requires special attention from eligible taxpayers when reporting under these schedules.

These schedules require detailed disclosures, consistency across multiple reporting sections, and alignment with supporting documentation to minimize audit exposure for resident taxpayers with offshore income, foreign tax credits, or offshore financial interests.

| Timetables | Key reporting considerations | Changes in ITR-1 and 2 for FY 2025-26 |

| Schedule of Foreign Source Income (FSI) and Tax Relief Schedule (TR) – ITR 2 | Taxpayers claiming the foreign tax credit must report foreign income by country and by source, along with the corresponding foreign tax paid/withheld Details such as the taxpayer’s identification number in the foreign jurisdiction, foreign tax reference details, the relevant article of the treaty (where applicable), and the exchange rate used for the conversion should be maintained. The amount claimed in Schedule TR must be reconciled with the income reported in Schedule FSI Form 67 must be filed to claim the foreign tax credit Make sure to maintain essential documents such as foreign payrolls, withholding statements, foreign tax payment receipts, foreign tax returns, etc. | No change |

| Schedule of Foreign Assets (FA) – ITR 2 | ROR taxpayers must disclose details of all foreign assets/financial interests held at any time during the year, including – foreign bank accounts, custodial accounts, equity interests/debts, foreign superannuation accounts, immovable property, trusts, and signature authority in foreign accounts Foreign asset balances will have to be reported on a calendar year basis, i.e. as on December 31, 2025. However, foreign income will be taxed and reported as per the Indian financial year. Maintain asset details such as country, name/address of institution or entity, account number/identification number, maximum balance/value of investment and income derived from it Incomplete or partial disclosure may result in audit notices and applicable penal consequences | In Schedule FA(G), reporting of income under “Business or Occupation” has now been removed. |

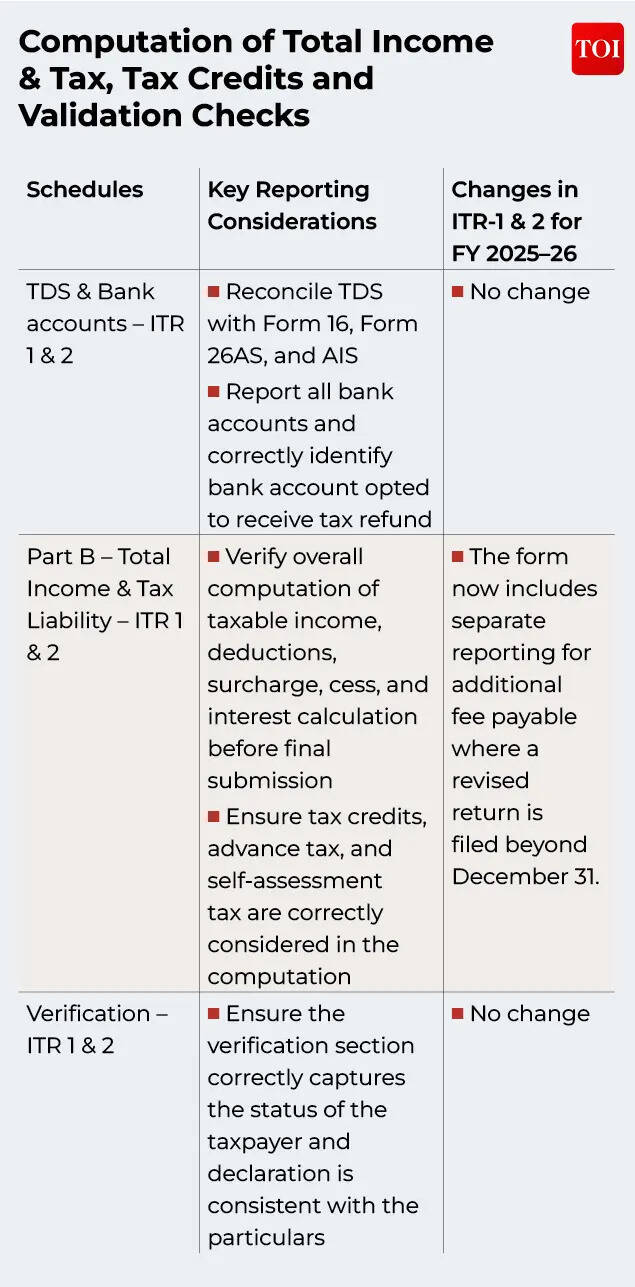

Calculate gross income, taxes, tax credits and validation checksThe concluding sections of the ITR form focus on computation of income from all principals, corresponding taxes on it, reconciliation of tax credits, and validation of data.

Taxpayers should carefully review these documents to ensure consistency with Form 26AS, AIS, TIS and supporting records before electronically filing the ITR.

Before proceeding with the application, taxpayers must ensure that the ITR form is free of verification errors. Any inconsistencies, incomplete disclosures, or incorrect ITR entries may result in validation errors in the utility, which must be resolved prior to electronic submission.Acting before the legal window closes: precision, preparedness, and accountabilityIn an increasingly digital tax landscape, ITR filing can no longer be treated as a routine year-end exercise based solely on Form 16 or tax deducted at source. Taxpayers should note that detailed instructions for completing notified IFR forms are still awaited and may provide further guidance on certain reporting requirements.In the above context, salaried taxpayers should begin their preparation well before the filing deadline by gathering supporting documentation, reconciling pre-populated information such as AIS and TIS, and carefully reviewing timeline disclosures to ensure accuracy and completeness.For most individual taxpayers, the due date remains July 31 after the end of the year except for individuals with business or professional income.

Delays can result in late filing fees, interest liabilities, limitations on the carry forward of certain losses, and slowed processing of refunds.Ultimately, in a system increasingly reliant on data matching, automation, and analytics, taxpayers who approach filing as a structured, proactive compliance exercise rather than a last-minute obligation will be much better positioned to avoid discrepancies, reduce risk, and ensure a smooth and efficient filing experience.(The author, Ravi Jain, is a tax partner at Vialto Partners. The article was also contributed by Vikas Narang, Director and Pawan Digha, Director at Vialto Partners. Views are personal)